Unabhängige Zeitung zu Wirtschaft und Verkehrspolitik

02:52 GMT+2

CENTRO INTERNAZIONALE STUDI CONTAINERS

ANNO XXXVIII - Numero SETTEMBRE 2020

MARITIME TRANSPORT

CONTAINER RATES ARE ON FIRE. HOW CAN YOU INVEST IN THAT?

Containers have wrestled the ocean-shipping headlines away from

tankers and bulkers as stratospheric China-to-California box rates

approach $4,000 per forty-foot equivalent unit (FEU). Container

shipping, declares a glowing new report by Fearnleys Securities, is

"The Unsung Hero."

How can investors expose themselves to this historic

trans-Pacific rate spike? Can box stocks woo tanker and bulker

shareowners? And what do the curiously low prices of some container

equities say about sentiment toward a U.S. recovery?

FreightWaves interviewed four shipping analysts to delve into

these questions. Their responses highlight significant differences

between investing in container shipping versus bulk commodity

shipping.

They also point to opportunities for investors and traders to

ride today's container wave.

Liner exposure

In tanker and dry bulk shipping, the ship owner is generally

U.S.-listed and extremely leveraged to highly volatile daily spot

freight rates. Theoretically, there should be a clear, direct link

between spot rates and stock prices.

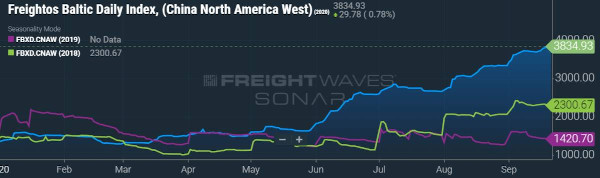

The link is not so clear in container shipping. According to the

Freightos Baltic Daily Index, spot rates from Asia to the U.S. West

Coast (SONAR: FBXD.CNAW) were up to $3,835 per FEU as of Monday. The

liner companies are the direct beneficiaries of these soaring spot

rates.

However, most liners have more long-term contract business than

spot business, and many own diversified logistics platforms.

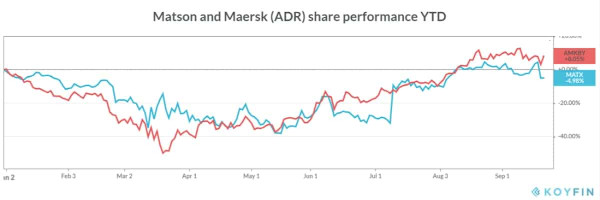

Meanwhile, almost all public liner companies are listed in Europe

and Asia, not the U.S.; the only U.S.-listed liner, Matson (NYSE:

MATX), is primarily in the domestic Jones Act trade.

Investing in global liner giant Maersk - which has two classes

of stock listed in Copenhagen and some thinly traded American

depositary receipts (ADRs) in the U.S. (OTC: AMKBY) - is a very

different proposition than, for example, buying Nordic American

Tankers (NYSE: NAT) shares on Robinhood.

Investors can also buy liner exposure through

U.S.-dollar-denominated bonds.

The prize goes to those who had the intestinal fortitude to buy

bonds of French liner CMA CGM at "peak fear" in March,

when those notes were trading at 55 cents on the dollar. They're now

close to par (100 cents).

Leasing: 'Not particularly sexy'

The primary way U.S. investors buy exposure to container

shipping is not through liners but via common and preferred shares

of leasing companies: ship owners that charter (rent) vessels to

liners and container-equipment owners that rent boxes to liners.

"It's kind of a boring business," acknowledged Ben

Nolan, analyst at Wells Fargo, referring to containership leasing.

"They're not particularly sexy," echoed Michael Webber,

founder of Webber Research & Advisory, of box-equipment lessors.

According to Randy Giveans, analyst at Jefferies, "When you

look at tankers, there's a lot more volatility in rates. More boom

and bust. With container shipping, utilization may move around a

couple of percentage points, and in normal times - and obviously

this year is not normal - rates stay in a pretty tight band. Plus,

there are a lot more vessels on long-term charters in the container

market than in tankers and dry bulk. Container shipping is more like

a conveyor belt moving goods from Asia to the U.S. and Europe.

"This year has been different. Because of COVID and the

massive supply and demand shocks to containers, it has been quite a

ride," said Giveans. "But usually, the driver for

containers is much more about global GDP. And the drivers for

tankers and dry bulk are more about geopolitical events and weather

and shocks to supply and demand."

Tanker and bulker stocks are generally more casino-esque than

the container stocks - and shipping investors have been more drawn

to the excitement of the casinos. Quite a few tanker stock buyers

have had a very exciting albeit very unprofitable year in 2020.

The case for ship lessors

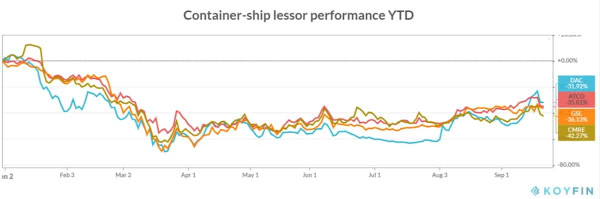

The U.S-listed containership lessors (otherwise known as tonnage

providers) include Seaspan owner Atlas Corp (NYSE: ATCO), Costamare

(NYSE: CMRE), Global Ship Lease (NYSE: GSL), Danaos Corp. (NYSE:

DAC), Capital Product Partners (NYSE: CPLP), Navios Containers

(NASDAQ: NMCI), Navios Partners (NYSE: NMM) and Euroseas (NASDAQ:

ESEA).

"There's a lot of misunderstanding of what these stocks are,"

said J Mintzmyer, analyst at Seeking Alpha's Value Investors Edge

(disclosure: Mintzmyer owns long positions in several containership

leasing stocks).

"This is just like aircraft leasing. Yes, there is a ship

and someone is steering the ship. But these are not actually

shipping companies.

"This is equipment leasing," he explained. "When

the liner industry is very healthy and counterparty risk goes toward

zero and interest rates are down, the value of the lease goes up."

Several analysts now argue that these stocks have not recovered

as much as they should have, contending that investors who buy in

now could pocket upside as the stocks catch up (even more so after

the recent days' sell-off).

These stocks have two main drivers, both of which are heavily

leveraged to the coronavirus. One is the counterparty risk of the

liners that charter the ships. In periods of crisis, liners have

defaulted and given the ships back. They have also renegotiated the

rates lower.

The second driver is charter maturities. If a lessor has ships

on 10-year charters, what's happening with charter rates this month

is irrelevant. But for a lessor with multiple charters expiring

soon, today's charter rates are highly relevant.

Charter rates, bond prices rebound

When liners "blanked" (canceled) double-digit

percentages of capacity from Asia to Europe and the U.S. during the

second quarter, they needed a lot fewer ships. Liners own a portion

of their fleet and charter the rest from tonnage providers. In

crisis periods when they need fewer ships, and a charter expires,

they'll either not renew or only renew at much lower rates.

During coronavirus, charter rates fell precipitously, by 25-40%.

Counterparty risks escalated. The stocks of the containership

lessors would logically sink on this combination - and they did.

Then, things went off-script. U.S. cargo demand was much higher

than expected and all the blanked capacity was reinstated.

Survivability fears about CMA CGM and other liners dissipated as big

second-quarter profits were reported. Bonds recovered.

Containership time-charter rates jumped all the way back to

where they were before the crisis began, in some cases higher.

Alphaliner reported Tuesday that rates for classic Panamaxes

(4,000-5,299 twenty-foot equivalent units) are now garnering their

highest rates since 2011 - up to $20,000 a day.

And yet, the stock prices of the containership lessors have not

followed suit. They're still down in the 30-40% range year to date.

According to Mintzmyer, "You can put up charts of all these

different things. The CMA bonds. The GSL bonds. Charter rates.

Maersk's stock. Matson's stock. The stocks of box lessors, companies

like CAI (NYSE: CAI). They're all correlated. January: great.

February, March: horrendous. Then recovery. But if you look at the

containership lessors, they're still all much closer to their

52-week lows."

Ship-lessor stocks left behind

Nolan at Stifel has been pointing out this disparity since

mid-August, dubbing containership leasing companies "the single

most compelling investment opportunity in traditional shipping

segments."

Nolan told FreightWaves, "You haven't seen the same degree

of follow-through [with prices] with respect to the ship-lessor

equities. The counterparty risk is off the table. The [charter]

rollover risk is less severe. The duration of time charters is going

up.

"The bonds have really rerated. So, either credit investors

[who bid up bonds such as CMA CGM's] are ahead of the curve or

they've missed something. Either there's a risk the bonds need to

come down or some of these equities need to come up."'

Battle for eyeballs'

There are at least two reasons the ship-lessor stocks haven't

recovered. One could be that there's not enough interest - these

stocks just aren't sexy enough. Another could be that there are

legitimate fears about the U.S. recovery.

"I think it's mostly a lack of air time," said

Mintzmyer. "If you look at tankers, what got those stocks

moving was companies speaking on CNBC and analysts talking about

those stocks."

Webber cited the "uphill battle for eyeballs" for

these stocks.

Nolan agreed that the container stocks have lacked attention.

"Capital for shipping is transient. Either it's there or it's

not. And right now, it's not. It doesn't really matter what you

think from a valuation perspective until there's a catalyst to get

people to want to look at it again. The question is: At what point

is there a catalyst? Maybe it will be [third-quarter] earnings.

That's my best guess at the moment."

Lag effect

Giveans and Nolan both said a lag between the surge in liner

spot container rates and containership lessor stock prices made

sense.

"When you see $4,000-per-FEU rates, the liners get that

cash immediately, whereas on the ship-charter side, the activity is

few and far between so you wouldn't see an immediate uplift [in

charter income]," said Giveans.

"It sort of makes sense that these [ship-leasing] equities

would lag because they're kind of the tip of the spear relative to

the liner companies," added Nolan.

"When there's excess capacity, the liners can lay off

equipment and still do reasonably well and the lessors bear the

brunt of that impact. Then, if the market begins to recover a bit

for the liners, it doesn't necessarily have to translate

[immediately] into a stronger market for the lessors."

But this raises the question: If stocks are inherently

forward-looking and efficient, the market should be able to account

for the charter-rate recovery as well as when lessors' charters will

expire (and reap the benefits of the rate recovery), then reprice

the stocks. If that's not happening, perhaps the market is pricing

in a faltering U.S. economic recovery?

Trouble ahead?

"The wild card here is that I don't think anybody can say

with high conviction that demand is going to be great for however

long," said Nolan. "It's surprisingly good now, but we're

not there yet."

"I think there are a lot of questions about the

sustainability of demand," said Giveans. "Container rates

are certainly going to come down as inventories get restocked and

demand doesn't rebound as quickly as many people had hoped."

"I think it reflects trepidation around the future,"

said Webber. "I agree that you would have thought there'd be

more of a recovery [in the containership lessor stocks]. But I also

think the markets are consciously or subconsciously inferring a

degree of credit risk."

Betting on box lessors instead

With containership lessors, said Webber, "the market

exposure is lumpy because you have bigger chunks of cash flow

rolling off at different times [due to charter expirations]. This

can overlap with the refi [debt refinancing] cycle, and all of a

sudden you get stuck."

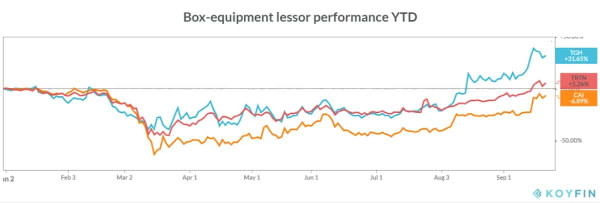

Webber believes a better way to invest in the container-shipping

space is to buy stocks in the box-equipment lessors that own

containers and rent them to liners (as with ships, liner companies

own a portion of their box fleet and rent the rest). These companies

include Triton (NYE: TRTN), CAI and Textainer (NYSE: TGH).

"They're more liquid [than shipping container stocks]. And

they don't have these waves of new supply that obfuscate what's

going on from a sector dynamics perspective like you do in

shipping," Webber explained.

It takes two years to build a ship but only six to eight weeks

to build a container. In practice, this means box supply is more

closely calibrated with demand than ship supply. It's less likely

for capacity owners to overshoot.

"These [box-equipment lessor] stocks offer a better

real-time gauge of what's actually happening from a trade

perspective, and they're closer as a real-time indicator to the

container lines themselves," argued Webber.

Investor interest still tepid

FreightWaves asked the analysts whether the recent publicity on

container-shipping spot rates is bringing more investors into the

fold.

Mintzmyer is enthusiastic. "It's so weird that nobody is

talking about this. I think container ships are the most interesting

of all the shipping sectors," he said.

"We have certainly had some calls," reported Giveans.

"But mostly from people who were already interested in

container ships. It's more legacy investors who had been on the

sidelines and are now saying, 'Oh my goodness, this market is

actually good. We have something positive here. How long can this

last?'

According to Nolan, "Whether this is inventory restocking

or stimulus spending or whatever, clearly something is going on. It

has raised some eyebrows. People are looking at it as a non-energy,

non-tech way to play the COVID-19 recovery. But it's certainly not

like my phone is ringing off the hook." Click for more

FreightWaves/American Shipper articles by Greg Miller