Independent journal on economy and transport policy

22:50 GMT+2

TRANSPORTATION

In 2022, the incidence of transport costs on the value of goods exported and imported from Italy rose for the third consecutive year

This is highlighted by the latest survey by the Bank of Italy on international transport

Roma

June 8, 2023

The Bank of Italy has published today the latest edition on 2022 of its survey on international freight transport of Italy, which is based on interviews conducted at 216 operators of international freight transport and presents Information mainly on mode-disaggregated freight rates transport and loading and carriers' market shares, distinguished by nationality. The results of the survey show a significant increase in transport fares concentrated in the first part of the year, which characterized almost all segments, mainly reflecting the expansion of international trade and higher fuel prices.

The analysis specifies that in some sectors have been added specific factors, such as the impact of geopolitical tensions on Transportation of oil and derivatives and limitations on the side of the supply in the maritime transport of containers, the latter failed in recent months. In addition, the report explains whereas in the presence of market shares of Italian carriers in slight Fall, the deficit in the balance of merchant transport of Italy grew further in 2022, reaching A new high.

According to the survey, in 2022 the incidence of transport costs on the value of goods exported and imported from Italy is rose for the third consecutive year, to 3.5 and 5.0 respectively percent (from 3.4 and 4.8 in 2021).

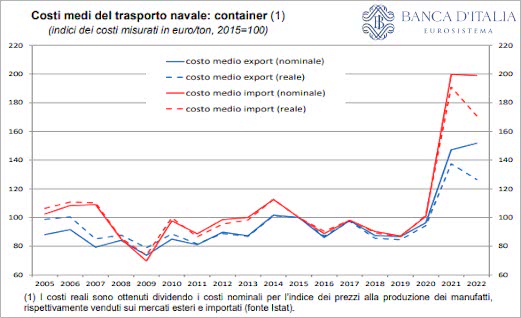

With regard to the maritime transport of containers, the survey points out that the freight rates recognised, net of ancillary services, have had in 2022 increases of limited magnitude in terms nominal compared to the previous year, characterized instead by exceptional increases. The average figure - the document specifies - hides However, a very different trend throughout the year, with factors that had caused it to rise in 2021 that have Recorded a trend reversal during 2022: First, there were significant reductions in the degree of concentration between shipowners, notes the Bank's document of Italy referring, in particular, to the announcement of MSC and Maersk not to renew their 2M alliance that will end at the end of 2024 ( of 25 January 2023), taking for granted (or having ascertained?) that the communication has already led to a diminution of the state of concentration of the containerized shipping market. To mark a reversal of the trend - the report points out - are There were also limitations on the supply side, including the Difficulties in finding containers and congestion in ports, as well as a slowdown in cargo demand and a its more balanced geographical distribution.

The examination of the Bank of Italy continues by specifying that "the freight dynamics were very heterogeneous in terms of geographical, affected by specific factors and precedents trends, with the most important flows (exports to North America and imports from China and other Asian countries) to drive average trends. The development of other cost factors (ancillary services) and the increase in average container loads (in a view to containing costs) - we read again - have induced a dynamic of total freight rates in euro per tonne very low, pushing costs in real terms to levels at below the highs recorded in 2021, but still high compared to previous years".

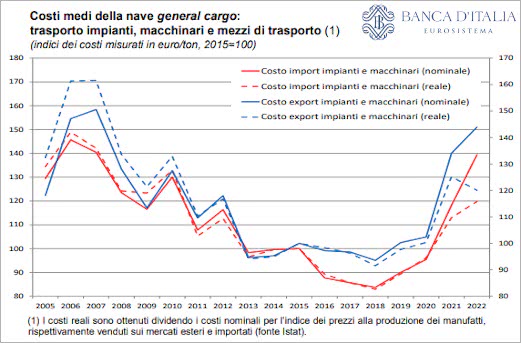

As regards the maritime transport of conventional and rolling stock, The survey finds that "in 2022 the average costs per tonne, including ancillary services, for the most relevant of general cargo (transport of "plants, machinery and means of transport") have increased in terms Nominal. In real terms, exports fell slightly and grown on imports, in both cases placing themselves on levels above the average of the last decade. In the remaining Types ("pipes and metallic materials" and "products chemicals, building materials, forest products") freight recorded high nominal growth rates of between 30 and 40 percent in both directions of flows, affected more than insufficient hold capacity than a demand for transport which, at least for the first part of the year, is has been supported. In the ro-ro sector - i.e. the naval transport of road vehicles with or without driver in tow, a segment of niche that concerns the Mediterranean area and with rates denominated in Euro - average costs fell in 2022, but with strong trends differentiated between the geographical areas concerned. In the face of increases in routes to and from France, Greece and Turkey, in fact, there are decreases in routes to and from Spain, the North Africa and the remaining Balkan countries".

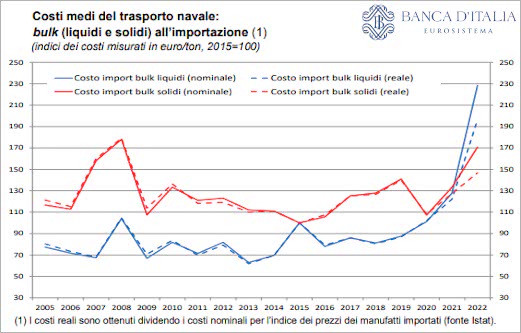

The document then examines the maritime transport of liquid and solid bulk observing that "for the quotations of the transport of solid bulk continued in the 2022 average the upward trend, both for grain and for the coal and minerals, in relation to economic developments and the related demand for raw materials. The war in Ukraine - the document specifies - has caused a greater instability of flows with consequent reverberation on costs, at least until the International Agreement on Exports of Cereals from that country. Similarly to transport by container ship, a First part of the year with growing freight rates followed a phase of decline. Average costs for handling chemicals (which include liquefied natural gas) recorded a rise almost in line with dry loads (around 30 percent); those for the transport of oil and derivatives have immediately a constant rise and overall magnitude high throughout the year, in relation to geopolitical tensions that have characterized the sector as well as the strong growth of imported volumes. Even in real terms average shipping costs import bulk (including ancillary services) related to solid loads are growing, although remaining below peaks recorded in 2008; those relating to liquid bulk have instead touched the maximum point in the period considered".

The survey, which has been conducted by the Bank of Italy since 1998, Since 2002 it has also carried out a sample survey aimed at Estimation of the breakdown of maritime freight transport to and from Italy between Italian and foreign carriers, analysis - points out the bank - which "constitutes a source of information not easily available internationally; In fact, the Available statistics often refer to the subject Ship owner and not to the actual operator, and Ship operator, on the basis of which it goes instead determined the residence for the purpose of compiling the balance of payments and to which the survey is therefore addressed samples". The latest survey explains that "in 2022 the Market shares by nationality of carriers have shown, at least for the main positions, little variation significant compared to the previous year. The most High container transport remains the prerogative of companies shipowners with Swiss control capital, while in transport bulk and general cargo continue to prevail Greek and Turkish shipowners respectively. In the ro-ro sector The highest share, close to 50%, goes to the Italians, whose weight is rather limited in the others components or even marginal as in the case of solid bulk. The Total average market share of Italian carriers, calculated weighting for transport costs - specifies the document again - fell slightly on the previous year (14.3 per year hundred, from 14.6). In the maritime sector it has remained almost unchanged, confirming an all-time low (7.1 percent); the Resumption of ro-ro and container shares was offset by declines in the remaining naval sectors. In a context of growth, after four years of reductions, of the fleet controlled and the volumes carried by resident shipowners, including The "foreign on foreign" handling activity is increased in quantitative terms returning to 2020 levels, with a consequent significant increase in its turnover".

With regard to road transport, the document notes that "In 2022 there was an increase of almost 20 per cent of the average road costs per tonne, which affected full and, to a greater extent, partial loads. In addition to the Significant increase in volumes handled, the increase is due to higher fuel prices, although low from government interventions, to the increase in maintenance costs and, indirectly, the entry into force of the Mobility Package for More restrictions applied. Almost all regions are were affected by the increase, with freight to and from the UK which were still affected by higher customs costs, and administrative following Brexit. Even in real terms - i.e. valued in relation to producer price indices manufactured goods sold on foreign or imported markets, respectively up 11.9 and 11.2 percent compared to 2021 - average road costs have grown, marking the value maximum since 2005 for those imported".

As for rail transport, it is noted that "in 2022 Average rail costs per tonne have increased in nominal terms in the container sector, while in the bulk sector have remained stable. Among the geographical areas, price increases have mainly concerned Central Europe and the Iberian Peninsula; the freight dynamics to and from Eastern Europe and the Balkans was much less intense due to some factors compensatory, such as the construction of longer trains and the adoption of modal shift incentives. Also in the railway The increase in energy prices has had repercussions, sometimes through the application of energy surcharges by operators, but this has not stopped the downward trend of average rail costs in real terms, which have returned to the 2012 lows".

Finally, for air transport, it is explained that "last Average air transport costs were moderate increase, concentrated in the first part of the year. The dynamic is was very heterogeneous geographically: the increases were very high freight rates to and from Asian countries (only export to China), against tariff reductions to and from Europe and North America. In real terms average costs have fallen but remain at high levels, after the exceptional Price increases in 2020 following the strong restriction of the supply of hold linked to the pandemic".

- Via Raffaele Paolucci 17r/19r - 16129 Genoa - ITALY

phone: +39.010.2462122, fax: +39.010.2516768, e-mail

VAT number: 03532950106

Press Reg.: nr 33/96 Genoa Court

Editor in chief: Bruno Bellio No part may be reproduced without the express permission of the publisher